Serving Hawaii State

Business Enterprise Valuation

Valuation of operating businesses where value is influenced by structure, control, and economic performance. Assignments include closely held companies, internal transactions, ownership transitions, and selected startup companies where valuation extends beyond standardized frameworks.

Analysis may include intangible assets and intellectual property, as well as valuation considerations arising in mergers, acquisitions, and related transaction structures. The focus remains on how enterprise value is formed, allocated, and supported under varying ownership and capital conditions.

Work is performed in accordance with recognized professional standards, including USPAP, and is prepared to support conclusions under review in financial reporting, tax, and transaction-related contexts. Engagements are selective and principal-led, based on the complexity of the valuation problem rather than routine or high-volume reporting.

Ownership Interests

Valuation of partial interests in entities where value is influenced by control, marketability, and structural characteristics.

Assignments commonly involve holding companies, layered ownership arrangements, and internal transfers where valuation must reflect the economic realities of ownership—not just underlying assets.

COMMERCIAL RE APPRAISAL & 50% Rule FEMA Appraisal

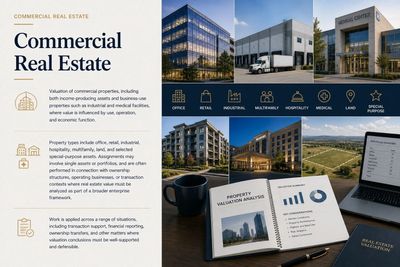

Commercial Real Estate

Valuation of commercial properties, including both income-producing assets and business-use properties such as industrial and medical facilities, where value is influenced by use, operation, and economic function.

Property types include office, retail, industrial, hospitality, multifamily, land, and selected special-purpose assets. Assignments may involve single assets or portfolios, and are often performed in connection with ownership structures, operating businesses, or transaction contexts where real estate value must be analyzed as part of a broader enterprise framework.

Work is applied across a range of situations, including transaction support, financial reporting, ownership transfers, and other matters where valuation conclusions must be well-supported and defensible.

FEMA Appraisal - 50% of the Market Value of the Building

The maximum improvement that can be made to the property without having to meet the FEMA Flood plain criteria is 50% of the value of the improvements.

If the cost of improvements or the cost to repair the damage exceeds 50 percent of the market value of the building, it must be brought up to current building codes including floodplain management standards. Thus, many property owners opted to do the renovation or damage repair not to exceed the 50% threshold. Most jurisdictions adopted the rule of 50% of the market value of the existing building improvements in the case of additional renovation, repair, or damage mitigation.

We can help assist you with your Substantial Improvement or 50% FEMA Rule Appraisal. The purpose of a 50% FEMA Rule is to promote redevelopment at or above the base flood elevation. In order to overcome this issue, one must determine the depreciated value of the improvements or the actual cash value (ACV) of the structure. Land value is not considered. Local building departments require a 50% FEMA Rule Appraisal or as it is often referred to an Actual Cash Value Appraisal of the improvements to determine if the scope of work on the commercial or residential property will be a Substantial Improvement.

That means an existing building must meet the requirements for new construction. People who own existing buildings that are being substantially improved will be required to make a major investment in them in order to bring them into compliance with the law.

COST SEGREGATION STUDY

Engineering-based cost segregation studies for commercial real estate, identifying components eligible for accelerated depreciation under current tax law.

With the restoration of 100% bonus depreciation for qualifying property placed in service after January 19, 2025, and expanded treatment of qualified production property under Section 168(n), cost segregation continues to provide significant timing benefits for capital recovery.

Analysis focuses on proper classification of assets into shorter recovery periods (e.g., 5, 7, and 15 years), supported by documentation prepared to withstand IRS review and coordination with tax advisors.

ESTATE AND GIFT TAX VALUATION

Assets for Gift and Estate Tax Planning

Valuation of closely held business interests, ownership interests, commercial real estate, and other assets in connection with estate and gift tax planning and reporting.

Assignments may involve family limited partnerships, limited liability companies, holding companies, partial interests, and underlying real estate or business assets where fair market value must be clearly supported.

Analysis may include discounts for lack of control and lack of marketability, with documentation prepared to support valuation conclusions under IRS review and related advisor coordination.

QUALIFICATIONS OF PRINCIPAL

David Hahn, CVA, MAFF, ASA, CM&AA, CCIM, MBA, has been in the Business Valuation, Cost Segregation Study/ Purchase Price Allocation Study, Renewable Energy Company Valuation, Capital Assets Valuation, Commercial Real Estate Appraisal, and other valuation appraisal practices since 1985. He is a principal of Alpha Appraisal Consulting Group, specializing in both intangible and tangible property types such as business, real, personal, contractual, intellectual and fractional properties.

David Hahn, ASA, CVA, MAFF, CM&AA, CCIM, MBA

· Economics, Appraisal, Valuation, & Consulting practices in multi-disciplinary assets including business, real estate, and fixed assets since 1985.

· Certified Business Valuation Analyst (CVA) credential from the (NACVA)

· Certified Commercial Investment Member (CCIM)

· Certified Merger & Acquisition Advisor (CM&AA)

· Master Analyst in Financial Forensics (MAFF) credential from the National Association of Certified Valuation Analysts (NACVA)

· Accredited Senior Appraiser designation of the American Society of Appraisers (ASA)

· Member of the American Academy of Economic and Financial Experts (AAEFE)

· Hawaii State Certified General Real Estate Appraiser #CGA-1171

· College Instructor's Credential - Business & Real Estate Instructor Certified through THE TRAIN THE TRAINER program - CCIM Institute

· Taught USPAP, Commercial & Business Appraisals, Financing, Commercial Investment, more than 5,000 classroom hours since 1985.

· Competent Toastmaster (CTM) certificate from Toastmasters International

· B.S. in Industrial Technology/Computer Science, Minor in Business - San Jose State University - 1981

· Control Data Corporation, San Jose, Business Systems Analyst, 1981-1983

· Lockheed Missiles and Space Company, Systems Analyst, 1983-1985

· Executive MBA - 1983 . USC, Public enterprise cost/benefit analysis graduate course, 1993

. UCLA Executive Management Program certificate - 1995

· Doctoral Studies, Public Administration, University of La Verne, 1995-1998

. U.S. Army veteran - active duty for 3 years - honorable discharge, 1979

DAVID HAHN Credentials